Annuity payout options are essential for individuals looking to secure their financial future. With various choices available, understanding these options can significantly influence your retirement strategy. Whether you’re considering a lump-sum payment or periodic disbursements, knowing the ins and outs of annuities can make a world of difference in achieving your financial goals.

This overview dives into the types of payout options, such as fixed and variable annuities, and highlights the critical factors that influence your decision-making process. From age and life expectancy to the tax implications of each option, we aim to equip you with the knowledge needed to navigate the world of annuities confidently.

Understanding Annuity Payout Options

Annuity payout options are a crucial aspect of retirement planning, offering investors various ways to receive their funds. Understanding the different types of payout options can have a significant impact on financial security during retirement. This discussion will delve into the various choices available, comparing lump-sum payments with periodic payments, and analyzing the implications of fixed versus variable annuities.

Types of Annuity Payout Options

Several payout options exist, each with specific characteristics that cater to different financial needs. The primary types of annuity payout options include:

- Lump-sum Payment: A single, large payment made to the annuitant. This option provides immediate access to the entire amount but requires careful planning to manage the funds effectively over time.

- Periodic Payments: Payments received on a regular schedule, which can be monthly, quarterly, annually, or at another specified interval. This choice can help with budgeting and offer a steady income stream.

Choosing between these options requires consideration of individual financial situations, spending habits, and expected longevity.

Comparison Between Lump-sum Payments and Periodic Payments

The decision between a lump-sum payment and periodic payments significantly influences financial security.

- Control Over Funds: With a lump-sum payment, the investor has complete control over the entire amount, allowing for potential investments or expenditures. However, this flexibility can lead to rapid depletion of funds if not managed wisely.

- Income Stability: Periodic payments offer a predictable income stream, reducing the risk of outliving one’s savings. This approach can enhance financial peace of mind, especially for retirees who prioritize consistent cash flow.

- Potential Returns: An investor who opts for a lump-sum may invest the funds, potentially yielding higher returns depending on market conditions. Nonetheless, this also involves higher risk compared to the security of periodic payments.

- Tax Implications: A lump-sum payment may result in higher tax liabilities in the year received, while periodic payments may distribute tax burdens more evenly over time.

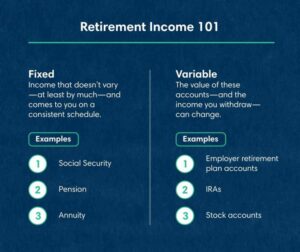

Fixed vs. Variable Annuities in Payout Options

Investors also face a choice between fixed and variable annuities, which carry different implications for payouts.

- Fixed Annuities: Provide guaranteed payouts based on predetermined rates, offering a reliable income stream regardless of market fluctuations. This option is ideal for conservative investors seeking stability.

- Variable Annuities: Allow payouts to vary based on the performance of underlying investments. While this option can lead to higher returns, it also entails greater risk, making it suitable for those comfortable with market volatility.

- Inflation Protection: Variable annuities may provide some measure of inflation protection through potential growth, while fixed annuities might lose purchasing power over time without cost-of-living adjustments.

- Complexity and Fees: Variable annuities can come with higher fees and complexities compared to fixed annuities, which may detract from overall returns.

Factors Influencing Annuity Payout Decisions

When selecting an annuity payout option, individuals face various considerations that can significantly impact their financial future. Understanding these factors is crucial for making an informed decision that aligns with personal circumstances and goals. Key elements such as age, financial aspirations, life expectancy, and tax implications play vital roles in shaping payout choices.

Age and Its Impact on Payout Choices

Age is a determining factor in choosing an annuity payout option. Younger individuals may prefer higher-risk investments with potential for higher returns, while those closer to retirement might lean towards stability and guaranteed income. As life expectancy increases, longer payout periods may be necessary, influencing the choice of fixed versus variable annuities.

Younger individuals (under 50)

Often opt for annuities that offer growth potential, such as indexed or variable annuities, to build a larger retirement fund.

Middle-aged individuals (50-65)

Tend to focus on balancing growth with security, potentially selecting a mix of fixed and variable options.

Older adults (over 65)

Usually prioritize guaranteed income to support retirement expenses, thus favoring immediate annuities or lifetime payouts.

Financial Goals and Objectives

The selection of an annuity payout option should align with specific financial goals, including retirement income needs, legacy planning, and investment growth. Individuals must assess their current financial status and future requirements to make suitable choices.

Income Generation

Those requiring steady income may choose lifetime annuities, which provide guaranteed payments for life.

Wealth Accumulation

Individuals focused on growth might select deferred annuities, allowing their investments to grow tax-deferred until withdrawal.

Legacy Considerations

For those wanting to leave an inheritance, options like joint-and-survivor annuities can ensure benefits continue for a spouse or other beneficiaries.

Life Expectancy and Payment Duration

Life expectancy is a critical factor influencing annuity payout decisions. Individuals with longer life expectancies may opt for payout structures that offer income over an extended period, while those with shorter life expectancies might choose lump-sum payments or immediate annuities.

Statistical Considerations

According to the Social Security Administration, a 65-year-old man has an average life expectancy of about 84 years, while a woman can expect to live to about 86. This data can guide choices regarding the length of payout periods.

Health Status

Personal health conditions and family medical history can also inform decisions on whether to opt for shorter-term versus longer-term payouts.

Tax Implications of Annuity Payout Options

Understanding the tax implications of various annuity payout options is essential for optimizing benefits and minimizing liabilities. Taxes can significantly affect net income received from annuities, depending on the type of annuity and the payout structure chosen.

Tax-Deferred Growth

Contributions to annuities typically grow tax-deferred. Taxes are only assessed upon withdrawal, which may serve to reduce current tax burdens.

Taxation on Payouts

Annuity payouts are subject to ordinary income tax. This means that the portion of the payout that represents earnings will be taxed, while the principal is not.

Lump-Sum Distributions

Choosing a lump-sum payout can trigger immediate tax liabilities, which may not be advantageous for individuals in higher tax brackets.

“Understanding your tax situation can help maximize the benefits of your annuity payouts.”

Exploring Life Annuities

Life annuities serve as a robust long-term income solution for retirees, allowing individuals to convert a lump sum of money into a steady stream of income for the rest of their lives. This financial product is designed to provide peace of mind, ensuring that retirees will not outlive their savings. By offering regular payments, life annuities help in managing the uncertainty surrounding longevity and the risk of depleting funds during retirement.A life annuity functions by requiring the policyholder to pay a premium, either as a lump sum or through multiple payments.

In return, the insurance company guarantees periodic payments to the annuitant for their lifetime, regardless of how long they live. This structure is particularly beneficial for those who have concerns about their longevity and the associated risk of outliving their financial resources.

Differences Between Single Life and Joint Life Annuities

Understanding the distinctions between single life and joint life annuities is crucial for making informed financial decisions. Below is a table summarizing the primary differences between these two types of annuities:

| Feature | Single Life Annuity | Joint Life Annuity |

|---|---|---|

| Definition | Provides income for one individual until death. | Provides income for two individuals, usually a couple, until both have passed away. |

| Payment Duration | Ends upon the death of the annuitant. | Continues until the second individual dies. |

| Payment Amount | Typically offers higher payments due to single coverage risk. | Generally offers lower payments than single life annuities, as the risk spans two lives. |

| Beneficiary Protection | No payments to beneficiaries after death, unless specified with a period certain option. | Can provide ongoing payments to the surviving spouse, offering additional financial security. |

The selection between a single life and a joint life annuity should be based on individual circumstances, including health, financial goals, and family considerations.

Benefits and Drawbacks of Life Annuities in Retirement Planning

Life annuities come with both significant advantages and potential downsides in the context of retirement planning. The following points provide a balanced view of their implications:Benefits:

Predictable Income Stream

Life annuities ensure that retirees receive a steady income, which can simplify budgeting and financial planning.

Longevity Risk Mitigation

By providing lifetime payments, life annuities reduce the anxiety associated with the risk of outliving savings.

Tax Advantages

Payments from life annuities may be taxed at a lower rate compared to regular income, depending on the annuitant’s tax situation.Drawbacks:

Lack of Liquidity

Once the premium is paid, accessing the lump sum can be challenging, limiting flexibility during retirement.

Inflation Risk

Standard life annuities may not provide protection against inflation, potentially reducing purchasing power over time.

Potentially Lower Returns

Depending on market conditions, the returns from life annuities might be lower than other investment options.Understanding these benefits and drawbacks helps retirees better assess whether life annuities align with their overall retirement strategy, ensuring they make informed decisions that suit their long-term financial needs.

Closing Summary

In conclusion, selecting the right annuity payout option is a pivotal aspect of financial planning that can provide stability and peace of mind during retirement. By weighing the benefits and drawbacks of each choice and considering your unique circumstances, you can make an informed decision that aligns with your long-term financial objectives. Ultimately, understanding your options will empower you to secure the retirement you envision.

Q&A

What are the main types of annuity payout options?

The main types include lump-sum payments, periodic payments, and life annuities.

How does age affect my choice of annuity payout?

Older individuals may prefer options that provide guaranteed income for life, while younger investors might opt for growth-oriented strategies.

What are the tax implications of annuity payouts?

Generally, annuity payouts are taxed as ordinary income, but tax treatment can vary based on the type of annuity and how it is funded.

Can I change my annuity payout option after choosing?

Most annuities have limited flexibility for changing payout options once selected, so it’s crucial to choose carefully.

What is the difference between fixed and variable annuities?

Fixed annuities offer guaranteed payments, while variable annuities are tied to investment performance, which can result in fluctuating payouts.